Blockchain Definition

What is Blockchain?

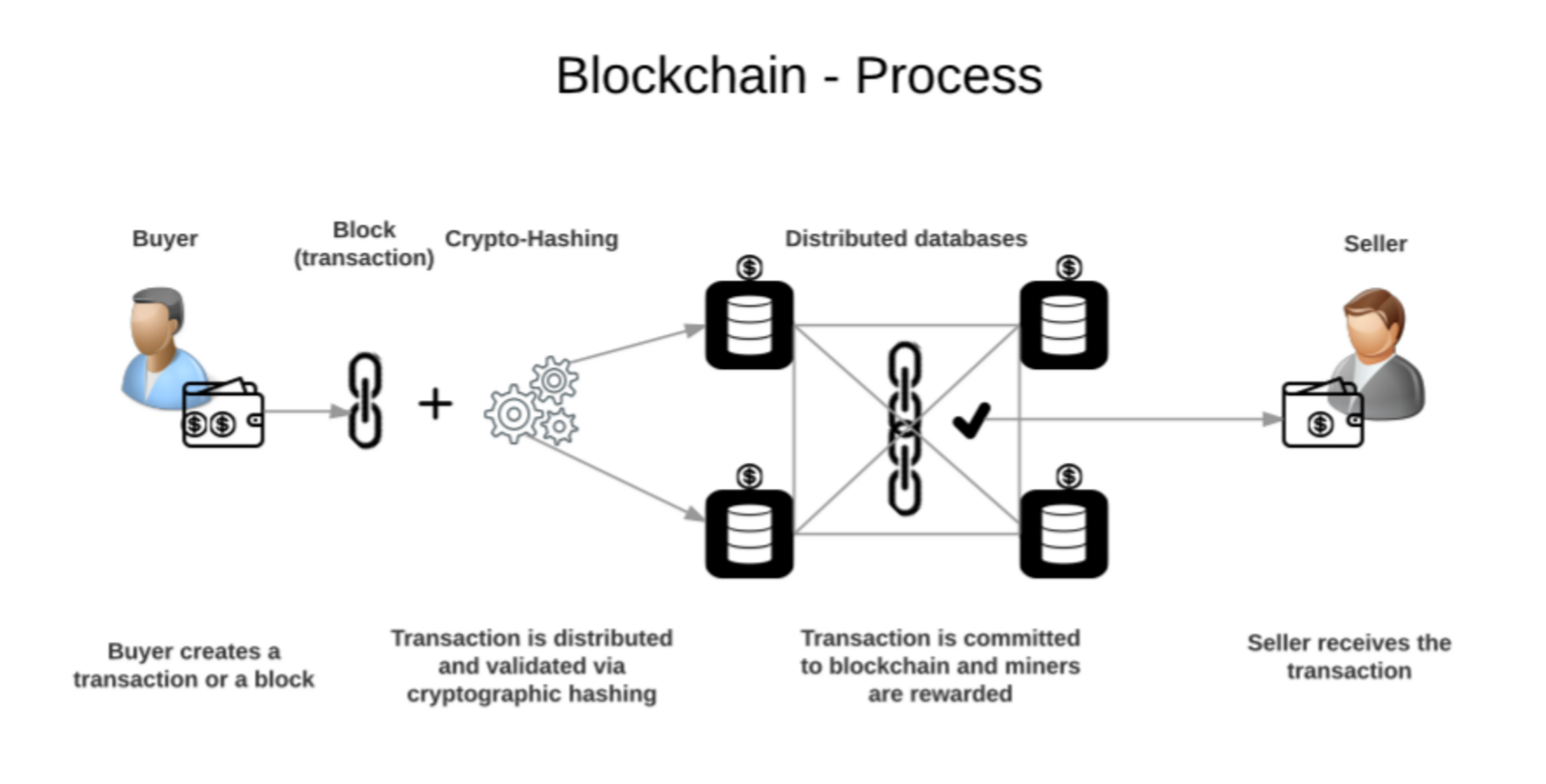

A blockchain is a digital, decentralized ledger that keeps a history of all transactions that occur on the blockchain’s network. This digital ledger is distributed to all users across a peer-to-peer network.

The network is designed so that whenever a new block of transactions is added to the ledger, it automatically updates for each user. Thus every node receives a full copy of the blockchain, no matter where they are in the world.

Blockchains can theoretically contain an infinite number of blocks, each linked together in a linear, chronological manner.

Because each transaction is timestamped when it is added to the blockchain, blockchain technology prevents users from double spending or manipulating transaction amounts.

Advantages of Blockchains

Blockchains have several distinct advantages as opposed to traditional databases and ledgers:

| Blockchain Advantages | |

| Digital | Blockchains can be accessed from anywhere in the world with an internet connection |

| Distributed | Each user has access to the same blockchain, allowing for greater transparency and auditability |

| Decentralized | Blockchains are not controlled by any central authority, but rather the totality of their users |

| Immutable | Transactions are timestamped and irrevocable - impossible to manipulate or forge |

| Cryptographic | Blockchains are secured through cryptography, so all data is securely stored and encrypted. |

Potential Applications for Blockchain Technology

The most common use for blockchains is in financial transactions. Blockchain technology is currently implemented within cryptocurrencies to verify every transaction that takes place on the network. Blockchains create a timestamped database that is updated every time a crypto coin is sent between two parties.

The decentralized nature of blockchains makes them especially helpful for international and cross-border payments. Low transaction costs, improved transparency, and quick settlement times make blockchain based payments much more desirable than traditional payment methods.

Blockchain technology can also be used in industries where record keeping is extremely important. Healthcare, manufacturing, and logistics are just a few examples because each of these industries relies on securing important information in an encrypted but accessible way.