What you need to know about the new Gemini Dollar (GUSD)

This week, Gemini Exchange announced a new token called the GEMINI Dollar, which is essentially an ERC20 token build on the Ethereum blockchain – representing an actual US Dollar. This US Dollar is held at a regular bank account – like any other USD.

Let me clarify two points before we continue.

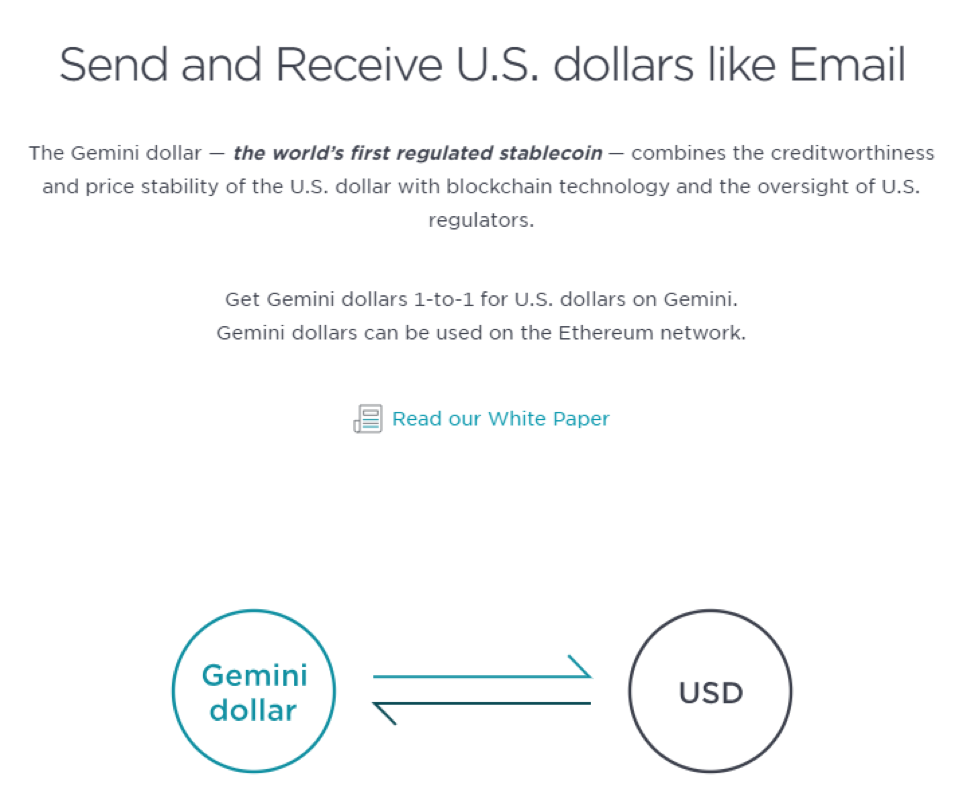

First, what Gemini has created here is an ERC20 token which lives on the open Ethereum network. Gemini will essentially issue this token whenever a user decides to convert their holdings into Gemini Dollar. This makes the token a stable-coin by definition, as the peg is always 1:1.

image taken from gemini.com

But that’s not the only unique feature of this token.

Once a verified Gemini user purchases the Gemini Dollar, the user is free to move it to any address he or she wishes on the public Ethereum network. This means that the user has complete freedom when it comes to the holding, transferring, buying and selling of this token. Since it is similar to the way one would move around Ether, it makes the Gemini Dollar act like cash on the blockchain.

More so, since the Gemini Dollar is a smart contract which runs on the Ethereum network, it frees the holder to use this token anywhere in the Ethereum ecosystem. Being a native token, it can be used by any dApp or service currently running on Ethereum. It will continue to gain more usability as the ecosystem is built.

The Future of the Gemini Dollar

This means any Gemini user can now send his Gemini Dollar easily and cheaply on the Ethereum network without going through a bank. This is revolutionary as it is the first time the USD lives on the Ethereum network as a tokenized asset. Think of it as digital cash (no pun intended).

Let’s imagine some use cases

P2P Transfers:

Two Gemini users can seamlessly send one another GUSD without going through Gemini, a bank, or any middleman. Unlike Venmo, Square or Paypal, the transaction is direct between these users (person to person) and requires no banking information or credit card processing.

P2P Transfers by Non-Verified Users:

Due to the public nature of the Ethereum ledger, there is nothing preventing a Gemini Dollar from being sent to other wallets, regardless of whether or not this user has been verified. This is an important aspect of the openness of Ethereum, as some will feel very comfortable holding Gemini Dollar even with no intention of ever cashing out. What they receive in return for holding their GUSD is the assurance that their asset is stable. and respected.

P2B Payments:

A business can sign up for Gemini and start accepting payments faster, without delays and with lower fees. It also makes duo of any hardware usually needed in Point-of-Sale business meant to for Credit Card clearing.

Online Commerce:

An online merchant can easily integrate an Ethereum wallet address into their website and allow anyone to pay with Gemini Dollar. An incredible amount of overhead can be saved for an online retailer in the process. No credit cards mean not paying for a third-party clearing services (such as Stripe or others).

Lending and Borrowing:

A lending site (such as EthLand, SALT, BlockFi) can integrate the Gemini Dollar with a few lines of code and allow users to lend and borrow seamlessly. This is easy since their infrastructure is already built on the Ethereum network.

Smart Payments:

Since the Gemini Dollar is a native to the Ethereum network, it can enjoy the smart capabilities given to it by developers. Take for example a smart contract which manages an automated parking lot and charges one’s account as it reads the license plate and opens the gate. The ability to make seamless payments and smart payments is a property only being made possible by the smart-contract infrastructure of the Ethereum blockchain.

Holding Gemini USD outside of a Bank:

The Gemini Dollar allows one to hold on to GUSD in a secure and private way – outside of the normal banking system. This is not merely a psychological: as the Gemini Dollar gains usability, so does the ability to keep using it outside of the usual banking infrastructure. Just like with cash, as long as trust is given in the system by the growing crowds, the need to exit the system reduces.

In addition to these use cases, we should point out a few of GUSD’s most valuable features:

- Stability and Trust: Many of our readers are familiar with the stable-coin Tether, whose sole purpose is to enable an escape route in stormy times. Ironically, few – if any – ever cash out Tether. Gemini Dollar does the same, but with one glaring difference: a higher level of trust. Gemini is a US-based exchange registered with all the regulatory bodies. This has extraordinary value in a system where trust is scarce.

- Transparency: Since the Gemini Dollar is just like any other ERC20 token, it enjoys the full transparency granted by the Ethereum public blockchain. While this can be seen as a deterrent for some, the majority of users can feel secure their ERC20 Dollar is visible, transferable, and viewable.

image taken from gemini.com

Gemini will continue to build trust as it adopts more users. It’s a snowball effect: the more users Gemini onboards, the more likely they are to use the Gemini Dollar. The more users adopt the GUSD, the more businesses are motivated to integrate it into their system.

The Sky is the Limit

we can’t fully know how will this programmable-economy will evolve and what new services will be offered. It’s also easy to imagine new businesses being built specifically with such integration, as it enables completely new cost-effective operations. Think of the effects of this as a large part of the US population moves to a native digital USD. The possibilities are endless.

Imagine how easily can Snapchat, Instagram, lyft, Uber and Fortnite integrate a this ERC20 USD token into their apps. Again, this isn’t just about making the current payment easier, it’s about the development of brand new payment options.

I can already envision a where we are using this new banking infrastructure, one in which crypto-exchanges are perceived the way we currently perceive banks. It is not a far-reaching thought to imagine Gemini or Coinbase as these new banks. These new banks will facilitate a new culture of openness, transparency, and respect for one’s accesso to an open financial system.

Combined, these exchanges will replace the banks and credit card companies in moving value seamlessly.